The theory of the consumer is used to explain the market demand for goods and services. The theory of the firm provides an explanation for the market supply of goods and services. A firm is defined as any organization of individuals that purchases factors of production (labor, capital, and raw materials) in order to produce goods and services that are sold to consumers, governments, or other firms. The theory of the firm assumes that the firm's primary objective is to maximize profits. In maximizing profits, firms are subject to two constraints: the consumers' demand for their product and the costs of production.

Consider a firm that produces a single good. In order to produce this good, the firm must employ or purchase a number of different factors of production. The firm's production decision is to determine how much of each factor of production to employ.

Variable and fixed factors of production. In the short‐run, some of the factors of production that the firm needs are available only in fixed quantities. For example, the size of the firm's factory, its machinery, and other capital equipment cannot be varied on a day‐to‐day basis. In the long‐run, the firm can adjust the size of its factory and its use of machinery and equipment, but in the short‐run, the quantities of these factors of production are considered fixed. The short‐run is defined as the period during which changes in certain factors of production are not possible. The long‐run is defined as the period during which all factors of production can be varied.

Other factors of production, however, are variable in the short‐run. For example, the number of workers the firm employs or the quantities of raw materials the firm uses can be varied on a day‐to‐day basis. A factor of production that can be varied in the short‐run is called a variable factor of production. A factor of production that cannot be varied in the short‐run is called a fixed factor of production. In the short‐run, a firm can increase its production of goods and services only by increasing its use of variable factors of production.

Total and marginal product. A firm combines its factors of production in order to produce goods or output. The total amount of output the firm produces, the firm's total product, depends on the quantities of factors that the firm purchases or employs. The marginal product of a factor of production is the change in the firm's total product that results from an increase in that factor by one unit, holding all other factors constant.

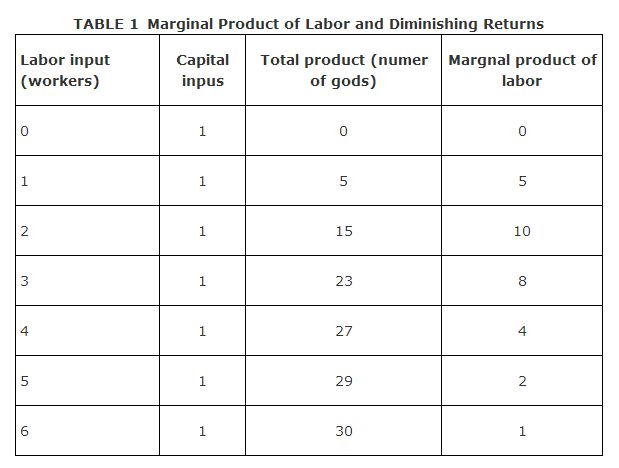

To better understand the concepts of total and marginal product, consider a firm that produces a certain good using only labor and capital as inputs. Assume that the amount of capital the firm uses is fixed at 1 unit. When the firm combines its fixed unit of capital with different quantities of labor, it is able to vary its output or total product. The change in the firm's total product, due to a 1‐unit increase in labor input, is referred to as the marginal product of labor.

Table provides a simple numerical example. When the firm combines its fixed unit of capital with one worker, its total product increases from 0 units to 5 units of the good. The marginal product of the first worker is therefore 5 (5 ‐ 0 = 5). If the firm adds a second worker, its total product increases to 15; the marginal product of the second worker is therefore 10 (15 ‐ 5 = 10). Continuing in this manner, it is possible to determine the marginal product of every worker that the firm hires.

Law of diminishing returns. The law of diminishing returns says that as successive units of a variable factor of production are combined with fixed factors of production, the marginal product of the variable factor of production will eventually decline. The law of diminishing returns is illustrated in Table . As more and more workers are combined with the firm's fixed amount of capital, the marginal product of labor eventually starts to decline; in Table , diminishing returns “set in” beginning with the third worker. Intuitively, if the firm's capital is fixed at 1 unit, the production possibilities of the firm are limited. Adding more and more workers cannot alleviate this situation and will eventually cause the marginal product of additional workers to fall. Note that diminishing returns is a short‐run phenomenon that will persist only as long as there are fixed factors of production; in the long‐run, it will be possible to vary the amount of the fixed factor capital so as to eliminate the problem of diminishing returns.